What's the outlook for Private Equity? Part 1

It's Industry Report season. Let's take a look at projections from Preqin, Bain Consulting, and others. Plus, commentary on Public Markets.

Report Season

We’re in the middle of two reporting phenomena: GPs are heads-down on Q4 Audit reporting and Consultants and Service providers are churning out their annual surveys and market landscape reports. While we can’t report on the former, the latter is chock-full of interesting content that is thankfully in the public domain. Below are links to our favorite reports and a few insights from across the industry.

Sentiment Surveys:

This GP-oriented report focuses on market conditions. As such, the picture they paint focuses on deal flow, maximizing asset performance, and incorporating investors’ impact goals into their strategies.

“Stakeholder attitudes are moving the goalposts”

Just click and read. Honestly can’t comment on the intent of this headline. It does indicate that the industry sees ESG as a component of fundraising rather than an important strategic endeavor.

Specialists can thrive despite large firm dominance in the space.

Club deals are coming back in vogue, thanks largely to increase purchase price multiples, but specialist funds also drive alpha because of their deeper sector expertise and more diverse networks.

This also gives us a chance to share one of the best industry white papers on PE investing, Cambridge Associates’ “Declaring a Major”… well worth your time!

Increasing fund sizes, despite being celebrated in industry publications, are causing concerns for investors, as are the increasing dry powder they inevitably contribute to.

The knock-on effect of inflated purchase price multiples is also a huge concern, being cited by 68% of respondents.

At the same time, the majority of respondents indicated that they are increasing allocations to Private Markets, which, of course, drives everything mentioned above.

Missed opportunity in this survey: Asking how likely respondents were to back first-time funds. This is complicated slightly by the fact that most respondents to this survey are Fund of Funds investors, but would still help solve the riddle of how to increase allocations without contributing to the bigger funds problem: back new funds and create more competition in the marketplace.

Other key themes:

Will this be the year that ESG breaks into the mainstream in Private Markets? There are three micro-trends that indicate the macro-trend is underway:

Service providers are adopting and enabling standards and releasing data products for free to Allocators.

Consultants are banding together to propose a new schema for data reporting.

GPs are publicly announcing their sustainability and ESG efforts. This is one area to watch, as it will be informed by the other two bullets…

The first Data Review of the Year: Pitchbook

According to Pitchbook’s data, YoY fundraising was flat from 2020 to 2021. It still indicates that $1.8tn was raised last year.

Private Markets AUM is $12tn as of 12/31/21, up from $10tn at the end of 2020

Interestingly, the early 2022 market correction will play a major role in one of the key metrics for measuring this year’s performance: Remaining fund value. If public market performance influences private asset marks, we could see a downtick. Obviously, the benefits of Private Markets investing are their lack of true correlation to Public, so any managers who aren’t under exit pressure will have more flexibility in the area of valuation.

Megafunds raised $143bn in 2021, up from $119 in 2020. Key drivers of dry powder and purchase price multiple issues.

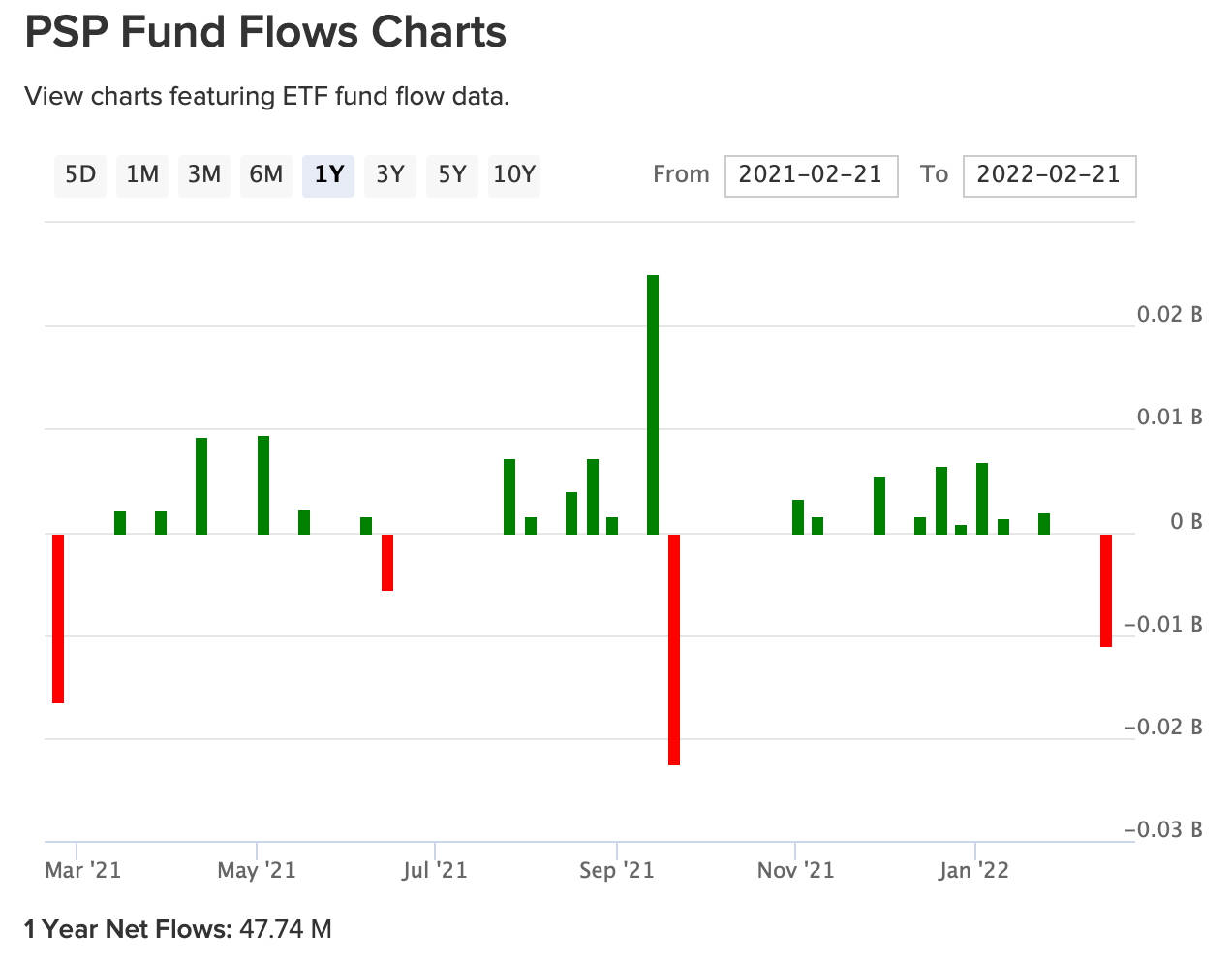

ETF Watch: $PSP

Public Markets

We’ve seen a lot of turmoil in 2022, but for the tech sector that turmoils started back in Fall of 2021. You can see here, that while the broader markets are down 10-15%, several individual stocks have plunged twenty or even fifty percent(!).

A lot of these tech companies are fundamentally good businesses and have still been brutally punished: Facebook, Salesforce.com, Zillow, Peloton. All with great products and loyal users…why the massive discount from the 52 week high?

Our take is that the landscape has changed…the frothy “growth at all cost” market is simply over. Investors want steady, certain returns more than moonshots and 50x acquisitions. On top of this, old habits die hard. If everyone in your company is used to gunning for growth, how will they feel once belts are tightened? Add to that, underwater stock options make it easier for key employees to jump firms and you can see why some of these stocks are trading where they are.

Us at 25

Nothing deep to say this letter. Keep taking risk even when you feel like you’re losing. If you zoom out over decades, a crypto bear market or a public markets correction will be a net positive if you’ve continued to invest through the mess. On the flip side, pulling the rip-cord near a market bottom can do the opposite. Need an anecdote? Here’s a tweet of someone trying to “market time” by selling their house 18mo ago….ouch!